as a gift

US

UK

- Phrase

- Given without expectation of payment; a present.

A2Moreas well as

US /æz wɛl æz/

UK /æz wel æz/

- Adverb

- Also; in addition to

- Preposition

- In addition to; and also.

A1Moreat risk

US

UK

- Phrase

- In danger; likely to be harmed

at the same time

US

UK

- Phrase

- Simultaneously; at the identical moment.

- Nevertheless; however; used to introduce a contrasting or qualifying statement.

A1Moreat work

US /æt wɚk/

UK /æt wə:k/

- Phrase

- Located at one's place of employment

A1Morebad habits

US

UK

- Noun (Countable/Uncountable)

- Negative or harmful routines or behaviors that are difficult to stop.

A1Morebased on

US

UK

- Phrasal Verb

- To use something as the foundation or starting point for something else.

- Preposition

- Using something as the main idea or foundation.

- Relying on something as evidence or justification.

A1Morebound

US /baʊnd/

UK /baʊnd/

- Transitive Verb

- To cover a wound, as with a bandage

- To put pages and a cover together to create a book

- Adjective

- (Papers) being kept together or covered

- Limited by a law, agreement, or contract

A2TOEICMorecome by

US /kʌm baɪ/

UK /kʌm bai/

- Phrasal Verb

- To become the owner of something, e.g. by accident

- To visit someone

A1Morecome up to

US

UK

- Phrasal Verb

- To meet expectations

A1Morecommitment

US /kəˈmɪtmənt/

UK /kə'mɪtmənt/

- Noun

- Permanent love or concern for person, thing

- Promise or decision to do something for a purpose

A2Moreconnected with

US

UK

- Phrase

- Related to; associated with.

- Involved with; having a relationship with.

- Phrasal Verb

- Was associated or linked to someone or something.

- Felt understanding or empathy with someone or something.

B1Moredefault

US /dɪˈfɔlt/

UK /dɪ'fɔ:lt/

- Noun (Countable/Uncountable)

- Automatic setting when no indicated preference

- Failure to meet an agreement or make a payment

- Verb (Transitive/Intransitive)

- To fail to meet as agreed; failure to pay

- To return to a previously determined state

B2TOEICMoreeconomic

US /ˌɛkəˈnɑmɪk, ˌikə-/

UK /ˌi:kəˈnɒmɪk/

- Adjective

- Concerning trade, industry, and money

- Financially worthwhile; profitable.

- Noun

- A system relating to economics

- A factor relating to economics

A2Moreface to face

US /fes tu fes/

UK /feis tu: feis/

- Adverb

- (Meeting) while looking at someone

A1Morefigure out

US /ˈfɪɡjɚ aʊt/

UK /ˈfiɡə aut/

- Phrasal Verb

- To understand the behavior of someone

- To think through logically to find a solution

- Verb (Transitive/Intransitive)

- To understand or find an answer to something.

- To find a solution to a problem or understand something.

A1Morefill out

US /fɪl aʊt/

UK /fil aut/

- Phrasal Verb

- To become fatter

- To complete a form by adding information needed

A1Morefinancial

US /faɪˈnænʃ(ə)l/

UK /faɪˈnænʃl/

- Adjective

- Involving money

- Relating to investments.

- Countable Noun

- A person who provides advice on financial matters.

A2TOEICMorefollow through

US /ˈfɑlo θru/

UK /ˈfɔləu θru:/

- Phrasal Verb

- To fulfill a promise

- Intransitive Verb

- To continue the motion of a stroke after hitting the ball, especially in golf or tennis.

A1Morefor example

US

UK

- Phrase

- As an illustration or instance.

for sure

US /fɔr ʃʊr/

UK /fɔ: ʃuə/

- Adverb

- Definitely; certainly; without a doubt.

- Used to emphasize a statement.

- Interjection

- An expression of strong agreement or affirmation.

A2Morefor the better

US /fɔr ði ˈbɛtɚ/

UK /fɔ: ðə ˈbetə/

- Phrase

- Resulting in improvement; to a more favorable condition.

A1Morefrom the first

US /frəm ðə ˈfɝst/

UK /frəm ðə ˈfɜ:st/

- other

- From the very beginning.

B2Morefrom the top

US /frʌm ði tɑp/

UK /frɔm ðə tɔp/

- Phrase

- From the beginning.

- From the highest point or position.

A1Morefuture self

US

UK

- Noun

- The person you will become in the future, often used in the context of making decisions that will benefit your future well-being.

- An idealized version of oneself that one aspires to become in the future.

A2Moreget around to

US /ɡɛt əˈraʊnd tu/

UK /ɡet əˈraund tu:/

- Phrasal Verb

- To finally start doing something you avoided doing

A1Morehave to

US /hæv tu/

UK /ˈhæv tə/

- Auxiliary Verb

- Must do

A1Morein a bubble

US /ɪn ə ˈbʌbl/

UK /ɪn ə ˈbʌbl/

- other

- Living isolated from reality or outside events.

B2Morein a nutshell

US

UK

- Phrase

- As a summary; including the main points concisely

C2Morein agreement

US

UK

- Adjective

- Sharing the same opinion or feeling.

- Having reached a mutual understanding or contract.

- Phrase

- Existing in harmony or correspondence.

B2Morein fact

US /ɪn fækt/

UK /in fækt/

- Adverb

- Used to emphasize the truth of a statement, especially one that contrasts with or contradicts something else.

- Used to introduce a more detailed or surprising piece of information.

- Phrase

- Used to emphasize the truth of a statement, especially one that is surprising or contrary to what might be expected.

C1Morein general

US /ɪn ˈdʒɛnərəl/

UK /in ˈdʒenərəl/

- Phrase

- Typically; usually; on the whole.

- Not specific or detailed; broadly.

- Adjective

- Not detailed or specific; overall.

C2Morein line with

US /ɪn laɪn wɪð/

UK /in lain wið/

- Phrase

- In agreement with; conforming to.

- In the same direction or alignment as.

- Preposition

- In agreement or conformity with.

A2Morein mind

US /ɪn maɪnd/

UK /in maind/

- Phrase

- Being aware of or considering something.

- To remember or consider something.

A2Morein order to

US /ɪn ˈɔrdɚ tu/

UK /in ˈɔ:də tu:/

- Preposition

- For the purpose of; with the aim of.

- Phrase

- In a specific sequence or arrangement.

- With the aim of; for the purpose of.

C1Morein particular

US /ɪn pɚˈtɪkjəlɚ/

UK /in pəˈtikjulə/

- Phrase

- Specifically; especially.

- Detailed or precise.

A1Morein the future

US /ɪn ði ˈfjutʃɚ/

UK /in ðə ˈfju:tʃə/

- Phrase

- At a later time; in times to come.

A1Morein the long run

US

UK

- Phrase

- Eventually; over a long period of time.

A1Morein with

US /ɪn wɪð/

UK /in wið/

- Phrase

- Fashionable or popular at the moment.

- Having influence or favor with someone.

- Phrasal Verb

- To introduce or bring something new into a system or organization.

A1Moreincentive

US /ɪnˈsɛntɪv/

UK /ɪnˈsentɪv/

- Noun (Countable/Uncountable)

- Something that encourages you to do something

- Adjective

- Serving to encourage or motivate.

B1TOEICMoreinteract with

US /ˌɪntɚˈækt wɪð/

UK /ˌɪntərˈækt wið/

- Phrase

- Verb (Transitive/Intransitive)

- To engage in communication or action involving mutual or reciprocal influence.

- To use a computer interface to achieve a specific goal.

A2Moreknow about

US /noʊ əˈbaʊt/

UK /nəʊ əˈbaut/

- Phrasal Verb

- To have information or understanding of a subject or situation.

lead to

US /lid tu/

UK /li:d tu:/

- Phrasal Verb

- To result in some action

- Verb (Transitive/Intransitive)

- To have something as a consequence or result.

A1Morelook at

US /lʊk æt/

UK /luk æt/

- Phrasal Verb

- To use your eyes to focus on something

- To focus your eyes on something carefully

A1Moreof course

US /ʌv kɔː(r)s/

UK /ɔv kɔː(r)s/

- Adverb

- Sure ; Certainly

- Phrase

- For sure; certainly

A2Moreof interest

US /əv ˈɪntrɪst/

UK /əv ˈɪntrəst/

- other

- Relevant or important to someone or something.

B2Moreon a day-to-day basis

US /ɑn ə ˈdeɪ tə ˈdeɪ ˈbeɪsɪs/

UK /ɒn ə ˈdei tə ˈdei ˈbeisis/

- other

- Happening regularly every day as a routine.

B1Moreon the line

US /ɑn ði laɪn/

UK /ɔn ðə lain/

- Phrase

- At risk; in a situation where something could be lost.

- Having a great deal of responsibility.

A1Moreon the other hand

US

UK

- Phrase

- Considering a different aspect of the matter; alternatively.

A1Moreopt in

US

UK

- Phrasal Verb

- To choose to participate in something; to give explicit consent.

A1Moreout of time

US /aʊt ʌv taɪm/

UK /aut ɔv taim/

- Adjective

- Having no more time available to do something.

A1Moreout there

US /aʊt ðɛr/

UK /aut ðɛə/

- Adverb

- In or to a place that is far away

- Existing in the universe

- Adjective

- Unconventional; strange; avant-garde

- Existing or available.

A1Moreover time

US /ˈovɚ taɪm/

UK /ˈəuvə taim/

- Phrase

- Gradually; as time passes.

- During a long period.

- Adverb

- Gradually; as time passes.

B1Moreover to

US

UK

- Preposition

- Used to hand over to someone else to speak

- The responsibility is now yours

participate

US /pɑ:rˈtɪsɪpeɪt/

UK /pɑ:ˈtɪsɪpeɪt/

- Intransitive Verb

- To take part with others in doing something

- To be involved in a discussion or conversation.

B1TOEICMorepay up

US

UK

- Phrasal Verb

- To pay money that you owe

A1Morepaying off

US

UK

- Phrasal Verb

- To give money to get person to do something; bribe

- To give money to settle a debt

- Verb (Transitive/Intransitive)

- To bribe someone.

- To result in success; to be worthwhile.

A1Morephone number

US

UK

- Countable Noun

- A sequence of digits assigned to a telephone subscriber, used to make a call to that phone.

A1Morepile up

US /paɪl ʌp/

UK /pail ʌp/

- Phrasal Verb

- To put things on top of each other to form a pile

- To increase in quantity or amount.

- Verb (Transitive/Intransitive)

- To accumulate or increase in quantity.

B1Morepoint out

US /pɔɪnt aʊt/

UK /pɔint aut/

- Phrasal Verb

- To make others aware of an idea

- To draw attention to something or someone

A1Moreput off

US /pʊt ɔf/

UK /put ɔf/

- Phrasal Verb

- To take off, e.g. clothing

- To delay until a later date

A1Moreput together

US /pʊt təˈɡɛðɚ/

UK /put təˈɡeðə/

- Phrasal Verb

- To build or assemble something small, e.g. a toy

- To organize or arrange something.

A1Morerather than

US

UK

- Adverb

- More exactly; more correctly

- Preferably; instead

- Preposition

- Instead of

A1Moreregardless of

US /rɪˈɡɑrdlɪs ʌv/

UK /riˈɡɑ:dlis ɔv/

- Phrase

- Preposition

- Without being affected or influenced by something; despite.

A2Morerely on

US /rɪˈlaɪ ɑn/

UK /riˈlai ɔn/

- Phrasal Verb

- To depend on someone or something

A2Moreresult in

US /rɪˈzʌlt ɪn/

UK /riˈzʌlt in/

- Phrasal Verb

- To cause or produce as a consequence.

rule of thumb

US /rul ʌv θʌm/

UK /ru:l ɔv θʌm/

- Noun (Countable/Uncountable)

- A practical and approximate way of doing or measuring something.

- A broadly accurate guide or principle, based on practice rather than theory.

A1Moresame time

US

UK

- Phrase

- Occurring simultaneously or at the same point in time.

- At the identical time as before; recurring at a fixed hour.

- Noun

- An equal duration or period.

A1Moresecurity

US /sɪˈkjʊrɪti/sə'kjurətɪ/

UK /sɪ'kjʊərətɪ/

- Noun

- Department in a company in charge of protection

- Financial document, like stocks, bonds and notes

A2TOEICMoreset up

US /sɛt ʌp/

UK /set ʌp/

- Phrasal Verb

- To make arrangements for something; establish

- Verb (Transitive/Intransitive)

- To arrange or prepare something for use.

- To start a business, organization, etc.

A1Moreshow up

US /ʃo ʌp/

UK /ʃəu ʌp/

- Phrasal Verb

- To arrive or be seen at a place, e.g. a party

- To be noticeably better than (someone else)

A1Moresign up to

US

UK

- Phrasal Verb

- To register for something, like a service or a course.

A1Morespend money

US /spɛnd ˈmʌni/

UK /spend ˈmʌni/

- Phrase

- To use money to buy or pay for something.

A1Morestudy for

US /ˈstʌdi fɔr/

UK /ˈstʌdi fɔ:/

- Phrasal Verb

- To prepare for an examination or test by learning and revising the subject matter.

such as

US /sʌtʃ æz/

UK /sʌtʃ æz/

- Preposition

- For example; like

A1Moretalking about

US

UK

- Phrasal Verb

- To discuss a particular topic.

- To be constantly mentioning or bringing up a subject.

A1Morethankful for

US

UK

- Adjective

- Feeling or expressing gratitude; appreciative.

- Grateful for a particular situation or benefit.

C1Morethanks to

US /θæŋks tu/

UK /θæŋks tu:/

- Preposition

- Because of; as a result of.

A1Morethe following

US

UK

- Adjective

- Next in order or sequence.

- Uncountable Noun

- What is about to be said or written.

B1Morethink about

US /θɪŋk əˈbaʊt/

UK /θiŋk əˈbaut/

- Phrasal Verb

- To consider something carefully.

- To remember or call to mind.

A1Morethink of

US /θɪŋk ʌv/

UK /θiŋk ɔv/

- Phrasal Verb

- To look on as (being something specific); consider

- To consider or remember something.

- Verb (Transitive/Intransitive)

- To imagine or call something to mind

A1Morethrough with

US

UK

- Phrase

- Having had enough (of trouble); wanting to stop

A1Moreto do with

US

UK

- Phrasal Verb

- To be about something; concern

A1Moreunder the assumption

US

UK

- Phrase

- Based on the belief or supposition that something is true.

A1Morework at

US /wɚk æt/

UK /wə:k æt/

- Phrasal Verb

- To have a job at a particular place or organization.

- To make an effort to improve something.

A1Morework in

US /wɚk ɪn/

UK /wə:k in/

- Phrasal Verb

- To make an opening for something in your schedule

- To fit person/thing into a schedule or sequence

A1More

Vocabulary

- think about: To consider something carefully.

- have to: Must do

- look at: To use your eyes to focus on something

- over to: Used to hand over to someone else to speak

- in the future: At a later time; in times to come.

- for example: As an illustration or instance.

- as well as: Also; in addition to

- rather than: More exactly; more correctly

- on the line: At risk; in a situation where something could be lost.

- lead to: To result in some action

- such as: For example; like

- in general: Typically; usually; on the whole.

- put off: To take off, e.g. clothing

- in order to: For the purpose of; with the aim of.

- talking about: To discuss a particular topic.

- in a bubble: Living isolated from reality or outside events.

- think of: To look on as (being something specific); consider

- in fact: Used to emphasize the truth of a statement, especially one that contrasts with or contradicts something else.

- of course: Sure ; Certainly

- opt in: To choose to participate in something; to give explicit consent.

- over time: Gradually; as time passes.

- study for: To prepare for an examination or test by learning and revising the subject matter.

- follow through: To fulfill a promise

- based on: To use something as the foundation or starting point for something else.

- set up

- show up: To arrive or be seen at a place, e.g. a party

- from the top: From the beginning.

- thankful for: Feeling or expressing gratitude; appreciative.

- at risk: In danger; likely to be harmed

- connected with: Related to; associated with.

- out there: In or to a place that is far away

- bad habits: Negative or harmful routines or behaviors that are difficult to stop.

- in a nutshell: As a summary; including the main points concisely

- at work: Located at one's place of employment

- under the assumption: Based on the belief or supposition that something is true.

- future self: The person you will become in the future, often used in the context of making decisions that will benefit your future well-being.

- in mind: Being aware of or considering something.

- rule of thumb: A practical and approximate way of doing or measuring something.

- spend money: To use money to buy or pay for something.

- fill out: To become fatter

- get around to: To finally start doing something you avoided doing

- at the same time: Simultaneously; at the identical moment.

- same time: Occurring simultaneously or at the same point in time.

- point out: To make others aware of an idea

- work at: To have a job at a particular place or organization.

- the following: Next in order or sequence.

- from the first: From the very beginning.

- for sure: Definitely; certainly; without a doubt.

- of interest: Relevant or important to someone or something.

- figure out: To understand the behavior of someone

- know about: To have information or understanding of a subject or situation.

- for the better: Resulting in improvement; to a more favorable condition.

- sign up to: To register for something, like a service or a course.

- regardless of

- paying off: To give money to get person to do something; bribe

- rely on: To depend on someone or something

- work in: To make an opening for something in your schedule

- pile up: To put things on top of each other to form a pile

- interact with

- result in: To cause or produce as a consequence.

- in the long run: Eventually; over a long period of time.

- through with: Having had enough (of trouble); wanting to stop

- pay up: To pay money that you owe

- put together: To build or assemble something small, e.g. a toy

- in particular: Specifically; especially.

- on a day-to-day basis: Happening regularly every day as a routine.

- as a gift: Given without expectation of payment; a present.

- on the other hand : Considering a different aspect of the matter; alternatively.

- face to face: (Meeting) while looking at someone

- come by: To become the owner of something, e.g. by accident

- in line with: In agreement with; conforming to.

- in with: Fashionable or popular at the moment.

- come up to: To meet expectations

- out of time: Having no more time available to do something.

- to do with: To be about something; concern

- in agreement: Sharing the same opinion or feeling.

- thanks to: Because of; as a result of.

- phone number: A sequence of digits assigned to a telephone subscriber, used to make a call to that phone.

- people: Persons sharing culture, country, background, etc.

- commitment: Permanent love or concern for person, thing

- decision: Choice made after thinking; final judgment

- security: Department in a company in charge of protection

- information: Collection of facts and details about something

- behavior: The way a person or thing acts; manner

- today: This day; day that is happening now

- financial: Involving money

- bound: To cover a wound, as with a bandage

- group: Two or more musicians who play music together

- incentive: Something that encourages you to do something

- default: Automatic setting when no indicated preference

- program: To make someone act or think in a certain way

- economic: Concerning trade, industry, and money

- participate: To take part with others in doing something

Get the full experience in the app

Learn anywhere with detailed sentence and usage analysis

01:03

She took a brave step forward, leaving behind her comfort zone to chase her dreams.

Vocabulary

- brave

adj. Having courage

- comfort zone

phr. A familiar situation where one feels safe

Explanation

a brave step is a noun phrase, where brave is an adjective modifying the noun step, meaning "a courageous step".

forward is an adverb modifying step, meaning "ahead".

The whole phrase serves as the object, answering the "what" of took (verb) — she took a brave step forward.

Get the full experience in the app

Look up words anytime with pronunciation, part of speech, and usage

brave

US/brev/

UK/breɪv/

adj.Brave

v.t.To bravely face

A2 Elementary

Get the full experience in the app

Practice speaking anytime and get instant pronunciation feedback

Try this speaking exercise.

Try practicing with this sentence.

80

WEBINAR: Behavior Economics 101

0

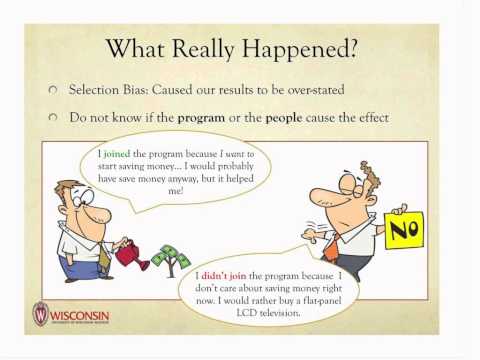

FlashJack posted on 2015/01/11Ever wonder why we make certain financial decisions? This webinar dives into the fascinating world of Behavioral Economics, showing you how 'default nudges' and 'commitment devices' can actually help us save more and spend smarter! You'll pick up practical vocabulary for everyday financial discussions and workplace scenarios.

Learn this video on the APP!

The VoiceTube App has more in-depth practice for videos!